There has been a very steep decline in the Canadian preferred share index in 2015 – so steep, in fact, that some investors are selling simply because their investment has lost value, which has to be one of the worst trade techniques ever (it imposes a form of negative convexity on your portfolio, among other bad things).

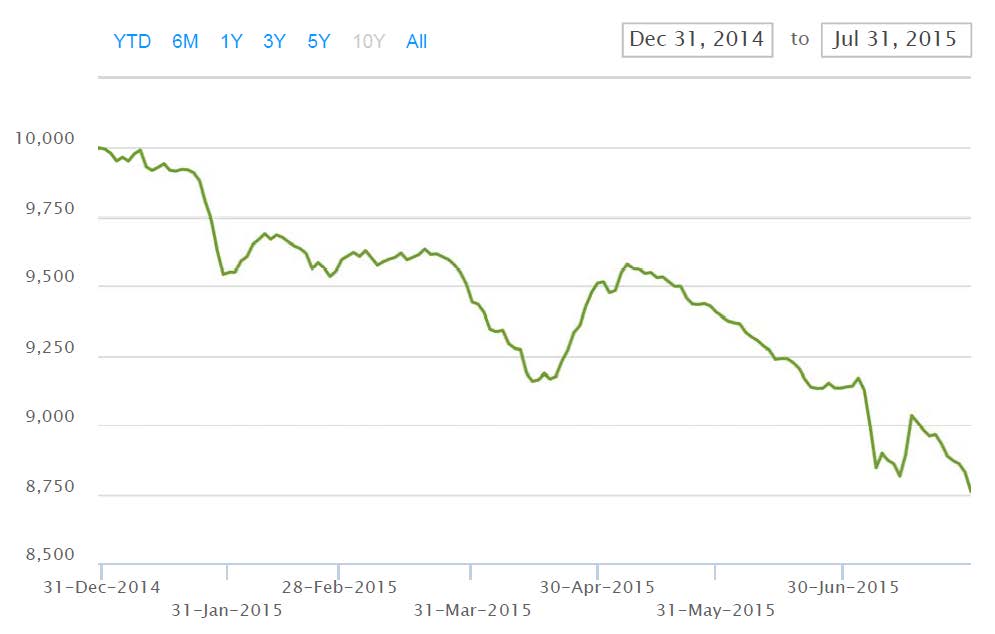

Still, it is unnerving. Look at the graph of the value of an investment in CPD, as published by Blackrock:

Click for big

Click for bigThis isn’t the smooth ride that some were expecting! The broad TXPR index was down 4.10% on the month and is down 11.47% over the past year. The FixedReset TXPL index has fared even worse, down 5.31% on the month and a horrific 17.26% on the year. I don’t have figures for the BMO-CM 50 at this time, but if I plug in the TXPR results for July, I can draw the following graph, which shows the rolling twelve month and twenty four month total returns from December 31, 1992:

Click for Big

Click for BigSo both the one- and two-year returns for the index now show losses exceeded only by the depths of the Credit Crunch in the 20+ years of data I have available. And, I will note, the four year total return for TXPR is now negative – in fact, you have to go back to January, 2011, to find a starting point that will give you a better than zero return through the period.

So I received an eMail from a client that said, in part:

But my real problem is that in trying to decide whether to stay in your fund or pull out, I do not know what I am betting on. The prospect of rising CDN interest rates (seems unlikely that would help), the overall Cdn economy? Something else?

What is your take on what it would take for preferred values to start moving in the right direction?

What follows is my answer, with minor edits to ensure anonymity and to reflect the medium of the message.

I can appreciate your concern.

Your first investment was valued on 2012-11-19; the second on 2013-1-21.

From the end of November, 2012, to June, 2015, the fund’s total return (reinvesting dividends, before fees) was -0.35%, compared to the BMO-CM “50” index return of -3.64%. TXPR (the broad S&P/TSX Preferred Share index) returned -4.04%, while TXPL (S&P/TSX, FixedResets only) returned -9.65%.

For the period beginning 2013-1-31 I find: Fund, -1.95%; BMO, -4.86%; TXPR, -5.56%; TXPL, -11.42%.

So the problem is not with the fund so much as it is with the market.

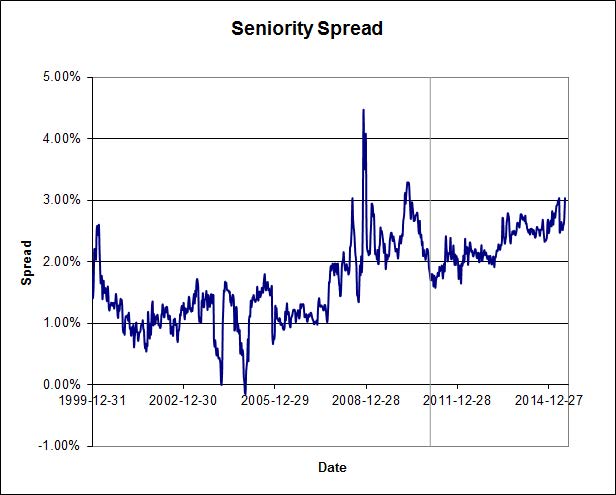

The indices are currently comprised of about 1/3 Straight Perpetuals, 2/3 FixedResets. For an idea of what has happened to Straights, see the attached Chart #22 from the July PrefLetter, which shows the interest-equivalent spread between Straight Perpetuals and long-term Corporate bonds (the “Seniority Spread”).

Click for Big

Click for BigMarket Yields changed as follows, from November 28, 2012 to June 30 , 2015

Five Year Canadas: 1.31% … 0.81%

Long Canadas: 2.38% … 2.37%

Long Corporates: 4.2% … 4.0%

Straight Perpetuals: 4.88% … 5.20%

Interest-Equivalent Straight Perpetuals: 6.35% … 6.76%

These changes have had the effect of widening the Seniority Spread from 215bp to 276bp. I can think of two rationales for this widening:

i) the retail investors who dominate the preferred share space are demanding a higher spread to compensate for perceived risks of losses once “interest rates start to rise”; that is, they are reacting more than the institutional investors in the bond market to risks of loss. This could be due to higher risk-aversion (defining “risk” as chance of loss), less binding duration constraints on the portfolio, simple lack of sophistication, or any combination of these three considerations. Note that I have not made a formal study of the subject and there may be other factors, but those are the ones that occur to me through my experience talking to investors.

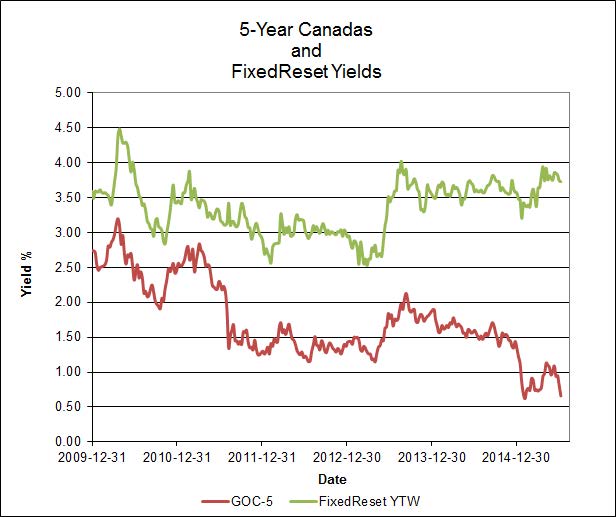

ii) Straight Perpetual yields are being pushed up (or at least supported) by FixedReset yields (see chart FR-44, below, from the extract from the July PrefLetter ). This would be due to a perception amongst investors that Straight Perpetuals are more “risky” (whatever that means!) than FixedResets and hence deserving of a positive spread; note that this effect is not observed when comparing sovereign inflation-indexed bonds to nominals (the Inflation Risk Premium).

Click for Big

Click for BigThese spreads use Yield-To-Worst, not Current Yield

This is Chart FR-44

With respect to FixedResets, it is clear from the horrible performance of TXPL referenced above relative to that of the broader TXPR (which one can approximate as being comprised of about 2/3 TXPL throughout the period of interest, although it has, of course, varied, with FixedReset issuance slightly overcompensating for capital losses) that FixedResets have been whacked.

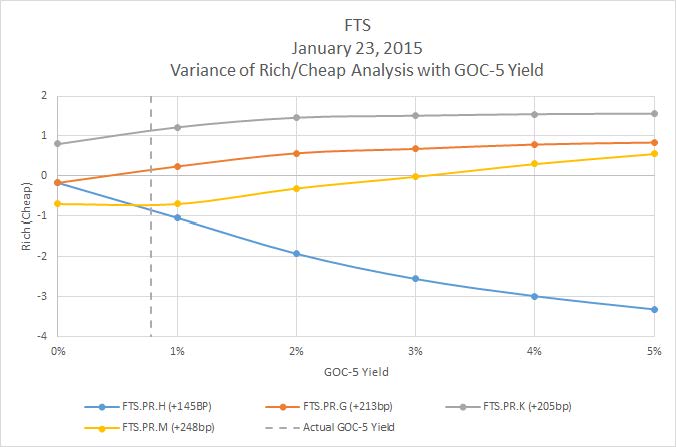

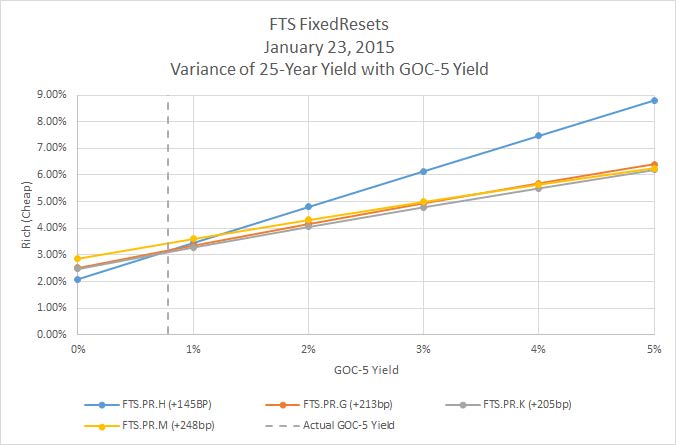

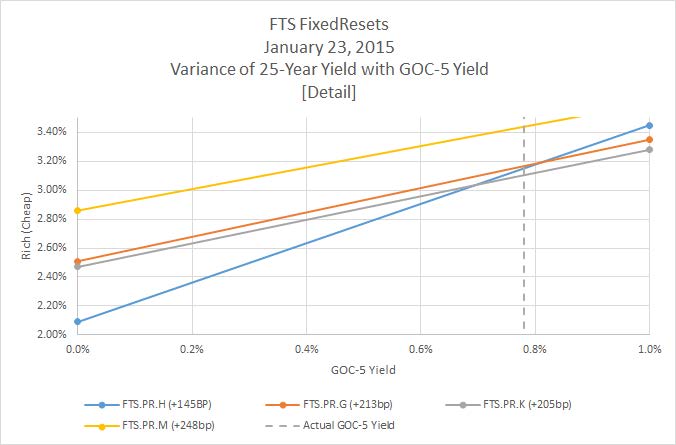

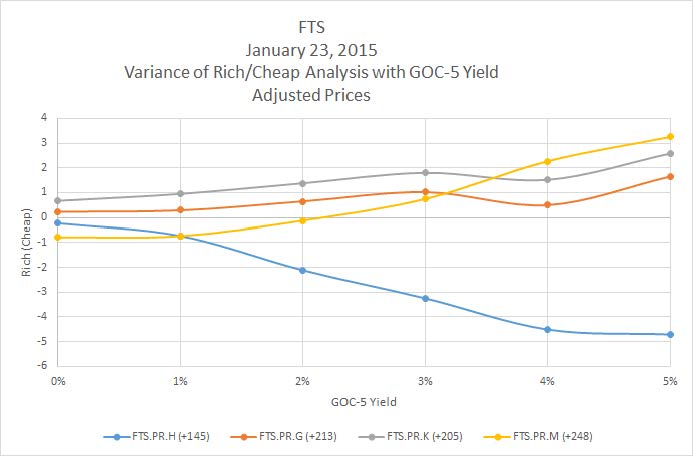

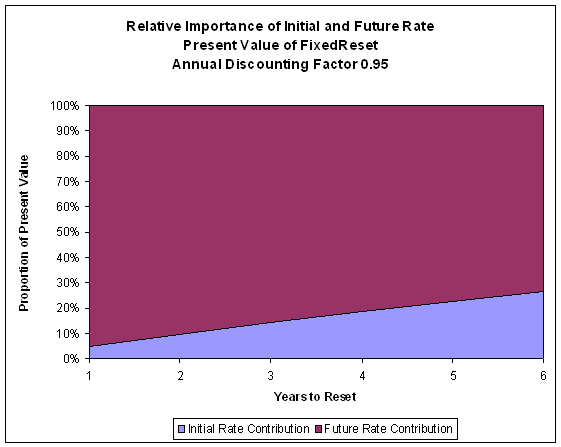

I have hypothesized a rationale for this underperformance in the attached extract from PrefLetter under the heading “An Experimental Data Series”, to wit: in the face of declines in the Five-Year Canada yield (which is the basis for the resets of of this type of preferred share), investors are attempting to maintain a constant yield irregardless of what is happening with other yields. This is hard to justify on rational grounds, but there has always been an element of irrationality in preferred share pricing! Thus, declines in the GOC-5 yield have been 100% compensated for by declines in price, without referencing yields of comparable long-term instruments; this contradicts one of the features of FixedResets that was used (perhaps inadvertently through indiscriminate use of the term “interest rates”) to help sell the issues when they were developed – that price would remain constant given parallel shifts in the yield curve (with credit spreads assumed, again implicitly, to be constant).

Click for Big

Click for BigThis 100% dependence of FixedReset price on GOC-5 has a very large effect, as derived in the last equation on page 3 of the extract:

i) The base Modified Duration of FixedResets is equal to (1 / EFCY). The term EFCY (“Expected Future Current Yield”) is about 3.75%, implying a Modified Duration of about 27 – not only far higher than long bonds, but dependent upon more volatile five-year yields to boot!

ii) The term (25/P) in the equation implies negative convexity

So to summarize, I feel that the poor performance of the market since your initial investment is due to:

i) very high dependence of FixedReset prices on GOC-5 levels, which has contradicted prior assumptions of an equal and opposite co-dependence on long-term yield levels.

ii) maintenance of a spread to PerpetualDiscounts, which has prevented Straight Perpetuals from participating in price increases due to declines in long-term corporate yields.

Click for Big

Click for BigThe “Bozo Spread” is the Current Yield of PerpetualDiscounts less the Current Yield of FixedResets

It is not yet clear whether the market pays more attention to these Current Yields, or to the Yields-to-Worst, when relating FixedResets to PerpetualDiscounts

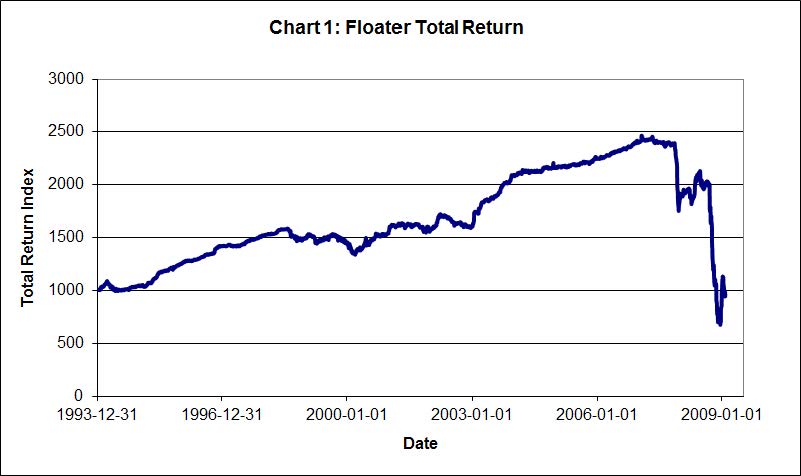

I will also note that to a certain extent, we’ve seen this movie before: during the Credit Crunch Floating Rate issues performed appallingly poorly, since their dividends were linked to contemporary (as opposed to expected!) Canada Prime while their yields were linked to PerpetualDiscounts (see my contemporary article and the next chart)

Click for Big

Click for BigNegative Total Return Over Fifteen Years!

So, while I can appreciate your dismay regarding the performance of your investment, I will point out that:

i) the key consideration is not past performance but how the characteristics of the asset class may be expected to fit into your portfolio requirements going forward.

ii) Expected income per unit in the fund has actually increased over the period, from $0.4643 in December 2012 to $0.5217 in June 2015 (see MAPF Performance: June 2015 ). This calculation is dependent upon various assumptions which you may or may not accept, but it represents my best guess!

iii) The increase in spreads over the period implies a significant reduction in expected income should you switch to another Fixed Income type of investment at this time.

iv) Expected future performance of FixedResets is highly geared to GOC-5, insofar as we can accept that the last equation on page 3 of the July PrefLetter extract reflects market reality. While I agree that we might be waiting a while for GOC-5 to increase substantially, I will suggest that current levels must be at or near a bottom. Mind you, I’ve been suggesting that continually for several years now and been wrong every time, so you may wish to disregard that particular exercise in market timing!

v) Expected future performance of Straights should be better than that of corporate long bonds over the medium term; and corporate long bonds should in turn outperform long Canadas; in both cases due to moderation of current high (by historical standards) spreads

I hope all this helps. I realize that I have used a fair bit of jargon in this eMail (and, what’s worse, jargon that I’ve developed myself!) so if there is anything in the above that makes no sense, feel free to ask for clarification. And, of course, if you would like to discuss this further prior to making an investment decision, that’s fine too – whether by eMail or telephone.

Sincerely,