It has been obvious for a while that a story like this would be coming … but it’s funny anyway:

Mr. Greenberg has been quietly building up a family of insurance companies that could compete with A.I.G. To fill the ranks of his venture, C.V. Starr & Company, he has been hiring some people he once employed.

Now, Mr. Greenberg may have received some unintended assistance from the United States Treasury. Just last week, the Treasury severely limited pay at A.I.G. and other companies that were bailed out by taxpayers. That may hasten the exodus of A.I.G.’s talent, sending more refugees into Mr. Greenberg’s arms, since C. V. Starr is free to pay whatever it wants.

“Basically, he’s just starting ‘A.I.G. Two’ and raiding people out of ‘A.I.G. One,’ ” said Douglas A. Love, an insurance executive who has also hired A.I.G. talent for his company, Investors Guaranty Fund of Pembroke, Bermuda.

…

Treasury officials said their special master for pay, Kenneth R. Feinberg, was aware that if he set pay standards that were too stringent, he could further harm A.I.G. by driving away its executives. “We’re acutely aware of this possibility,” said Andrew Williams, a department spokesman. “That’s why Ken Feinberg spent hours at A.I.G. trying to understand that specific dynamic and strike the right balance.”

Hours. What dedication! What thoroughness!

Mark Carney has come up with a good illustration of the intellectual bankruptcy of many of the current regulatory efforts:

Financial institutions need to demonstrate an awareness of their broader responsibilities. Financiers should ask themselves every day how their activities affect systemic risk? and what are they doing to promote economic growth?

Oh, yeah? Who’s going to pay them to do this? Who’s going to give them a look at the books of their counterparties? Who’s going to give them power over their counterparties? This is just another cheap attempt to shield regulators from responisibility for the consequences of their actions.

And there may be consequences: Roubini thinks another bubble is forming:

Investors worldwide are borrowing dollars to buy assets including equities and commodities, fueling “huge” bubbles that may spark another financial crisis, said New York University professor Nouriel Roubini.

“We have the mother of all carry trades,” Roubini, who predicted the banking crisis that spurred more than $1.6 trillion of asset writedowns and credit losses at financial companies worldwide since 2007, said via satellite to a conference in Cape Town, South Africa. “Everybody’s playing the same game and this game is becoming dangerous.”

On the other hand, the new paradigm means that employer cartels can cloak themselves in holiness:

JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon said he won’t actively recruit the best employees from competitors operating under pay restrictions imposed after federal bailouts.

“I morally have an issue with people going against those companies that are hamstrung,” Dimon said today at the Securities Industry and Financial Markets Association meeting in New York. “It’s wrong to say, ‘Let’s go hire the best people.’ We’re not going to do that.”

It’s wrong to compete! It’s wrong to put the boots into your competitor when he’s down!

John Mackie has written an interesting piece about bond indentures, Bonds’ Bold Terms: Bonds Rule, With Banks Out

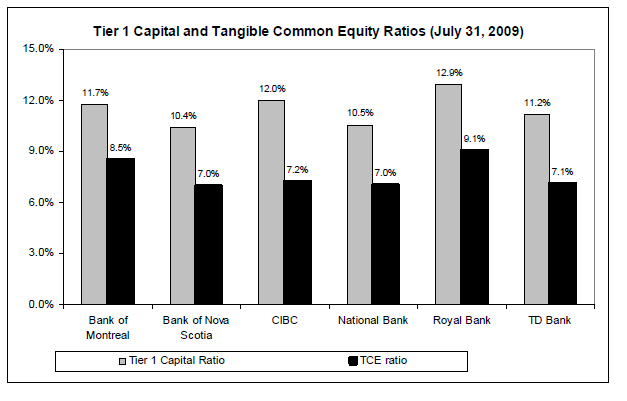

Despite all my efforts, there are still a few misguided souls out there who believe that Credit Rating Agencies should predict future economic conditions; some of these even believe that if they don’t do it better than the Fed, it must be because they are either corrupt or incompetent and probably both. DBRS has today released its overview of Canadian credit markets, with slides from presentations on structured finance and the outlook for 2010 and beyond. The forecasts have the usual quota of entertainment value; there are a few interesting charts:

Click for big

Back to normal for preferreds, with PerpetualDiscounts losing 14bp on the day and FixedResets down fractionally. Volume was normal – OK, maybe off a bit – but the volume highlights were dominated by straights.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6470 % | 1,469.4 |

| FixedFloater | 6.43 % | 4.52 % | 46,309 | 18.18 | 1 | 2.9860 % | 2,421.2 |

| Floater | 2.65 % | 3.09 % | 110,622 | 19.50 | 3 | -0.6470 % | 1,835.8 |

| OpRet | 4.87 % | -6.81 % | 115,411 | 0.09 | 15 | 0.1845 % | 2,293.6 |

| SplitShare | 6.41 % | 6.45 % | 482,876 | 3.94 | 2 | -0.0221 % | 2,063.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1845 % | 2,097.3 |

| Perpetual-Premium | 5.89 % | 5.92 % | 140,830 | 13.92 | 11 | 0.2387 % | 1,857.1 |

| Perpetual-Discount | 5.99 % | 6.06 % | 217,339 | 13.84 | 63 | -0.1441 % | 1,732.7 |

| FixedReset | 5.53 % | 4.23 % | 451,614 | 4.00 | 41 | -0.0064 % | 2,106.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 12.60 Evaluated at bid price : 12.60 Bid-YTW : 3.14 % |

| PWF.PR.E | Perpetual-Discount | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 21.93 Evaluated at bid price : 22.28 Bid-YTW : 6.19 % |

| BAM.PR.P | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-30 Maturity Price : 25.00 Evaluated at bid price : 26.55 Bid-YTW : 5.74 % |

| BMO.PR.K | Perpetual-Discount | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 22.49 Evaluated at bid price : 22.62 Bid-YTW : 5.91 % |

| RY.PR.G | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 19.38 Evaluated at bid price : 19.38 Bid-YTW : 5.82 % |

| GWO.PR.I | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 6.23 % |

| ENB.PR.A | Perpetual-Premium | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 24.69 Evaluated at bid price : 25.01 Bid-YTW : 5.58 % |

| POW.PR.B | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 21.52 Evaluated at bid price : 21.85 Bid-YTW : 6.16 % |

| IGM.PR.A | OpRet | 2.47 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2009-11-26 Maturity Price : 26.00 Evaluated at bid price : 27.40 Bid-YTW : -46.86 % |

| BAM.PR.G | FixedFloater | 2.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 25.00 Evaluated at bid price : 16.90 Bid-YTW : 4.52 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.A | FixedReset | 82,010 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-30 Maturity Price : 25.00 Evaluated at bid price : 25.33 Bid-YTW : 4.41 % |

| BMO.PR.L | Perpetual-Premium | 42,630 | RBC bought 15,000 from Nesbitt at 25.05. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 24.69 Evaluated at bid price : 24.91 Bid-YTW : 5.92 % |

| BNS.PR.O | Perpetual-Premium | 31,300 | RBC crossed 21,700 at 24.41. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 24.09 Evaluated at bid price : 24.30 Bid-YTW : 5.79 % |

| IAG.PR.A | Perpetual-Discount | 29,400 | RBC crossed 23,600 at 19.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 6.18 % |

| RY.PR.A | Perpetual-Discount | 29,371 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 19.29 Evaluated at bid price : 19.29 Bid-YTW : 5.78 % |

| CM.PR.I | Perpetual-Discount | 28,055 | RBC crossed 11,200 at 19.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-10-27 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 6.07 % |

| There were 45 other index-included issues trading in excess of 10,000 shares. | |||